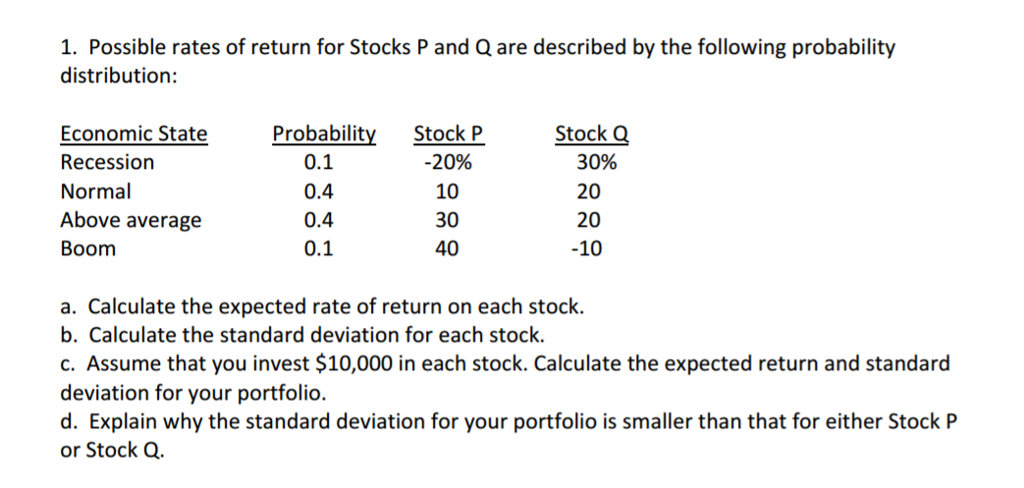

It is important to understand your credit score before you can get a loan. There are many credit scoring systems. These include FICO 10, VantageScore and the UltraFico. Learn how to interpret your score, and how it affects your financial health.

Score with Experian UltraFICOTM

Experian, which created the FICO credit score is about to launch its new score. The new UltraFICO model will give consumers a better view of their credit score. It is especially relevant for consumers with poor credit scores, or those who have had mistakes in their credit history.

UltraFICO (tm), a score that uses information compiled directly from consumer bank statements, calculates credit risk. To create an overall score, this information is combined with Experian credit information.

VantageScore

VantageScore comprises six credit types. These categories include your credit history, payment history, age, type of credit, amount owed, and credit behavior. Your score will be impacted if late or missed payments are made. There are several ways to increase your credit score.

One way to improve your score is to reduce your collection accounts. Medical collections aren't considered as dangerous as other collection accounts. If medical collections are less than six-months old or were intended to be paid by an insurance company, they may be ignored.

FICO 10

FICO 10, also known as the T score, is a new credit scoring system. The new model examines a snapshot rather than the whole credit report. This model will do a better job of separating high-risk and low-risk consumers. FICO 10 scores will increase if you have high credit. Bad credit will result in a lower score. This is normal with a new credit scoring system.

To improve your FICO 10, you should make sure that you pay off all your credit cards in full each monthly. Your credit utilization (the percentage of your credit card balances that are higher than the total amount of credit card credit) will be lower. A higher credit limit is also possible. The previous FICO score factored late payments into your credit score, but the new FICO 10 score takes trended data into account.

Resilience Index

The Resilience Index is a new credit score created by FICO and is available for free to lenders. This tool can help lenders predict consumer resilience before they approve credit applications. Although it's free to lenders, it's not yet available for the general population.

The Resilience Index measures how resilient consumers are to financial stress. This rating is more detailed than a simple credit score, and it can help lenders make better decisions during financial instability. It is possible to help lenders continue lending money to consumers with high credit scores, while limiting risk for those with lower credit scores. It allows lenders to increase their eligibility requirements when opening new accounts. These features are especially useful in today's turbulent economic climate.

FAQ

Do I invest in individual stocks or mutual funds?

Mutual funds can be a great way for diversifying your portfolio.

They are not suitable for all.

You shouldn't invest in stocks if you don't want to make fast profits.

Instead, you should choose individual stocks.

You have more control over your investments with individual stocks.

Online index funds are also available at a low cost. These funds allow you to track various markets without having to pay high fees.

How do I wisely invest?

You should always have an investment plan. It is important to know what you are investing for and how much money you need to make back on your investments.

Also, consider the risks and time frame you have to reach your goals.

This will allow you to decide if an investment is right for your needs.

Once you have decided on an investment strategy, you should stick to it.

It is best not to invest more than you can afford.

Do I need any finance knowledge before I can start investing?

No, you don’t have to be an expert in order to make informed decisions about your finances.

You only need common sense.

That said, here are some basic tips that will help you avoid mistakes when you invest your hard-earned cash.

Be careful about how much you borrow.

Don't fall into debt simply because you think you could make money.

Also, try to understand the risks involved in certain investments.

These include inflation and taxes.

Finally, never let emotions cloud your judgment.

Remember that investing isn’t gambling. To be successful in this endeavor, one must have discipline and skills.

This is all you need to do.

Which type of investment yields the greatest return?

The answer is not necessarily what you think. It depends on what level of risk you are willing take. If you put $1000 down today and anticipate a 10% annual return, you'd have $1100 in one year. Instead, you could invest $100,000 today and expect a 20% annual return, which is extremely risky. You would then have $200,000 in five years.

In general, the higher the return, the more risk is involved.

It is therefore safer to invest in low-risk investments, such as CDs or bank account.

This will most likely lead to lower returns.

High-risk investments, on the other hand can yield large gains.

A 100% return could be possible if you invest all your savings in stocks. But it could also mean losing everything if stocks crash.

Which one do you prefer?

It all depends on what your goals are.

You can save money for retirement by putting aside money now if your goal is to retire in 30.

But if you're looking to build wealth over time, it might make more sense to invest in high-risk investments because they can help you reach your long-term goals faster.

Remember: Higher potential rewards often come with higher risk investments.

But there's no guarantee that you'll be able to achieve those rewards.

What are some investments that a beginner should invest in?

Start investing in yourself, beginners. They should learn how to manage money properly. Learn how to save for retirement. How to budget. Learn how you can research stocks. Learn how to read financial statements. Learn how to avoid scams. Make wise decisions. Learn how diversifying is possible. Learn how to protect against inflation. Learn how to live within ones means. How to make wise investments. This will teach you how to have fun and make money while doing it. You will be amazed at what you can accomplish when you take control of your finances.

Statistics

- 0.25% management fee $0 $500 Free career counseling plus loan discounts with a qualifying deposit Up to 1 year of free management with a qualifying deposit Get a $50 customer bonus when you fund your first taxable Investment Account (nerdwallet.com)

- Some traders typically risk 2-5% of their capital based on any particular trade. (investopedia.com)

- They charge a small fee for portfolio management, generally around 0.25% of your account balance. (nerdwallet.com)

- If your stock drops 10% below its purchase price, you have the opportunity to sell that stock to someone else and still retain 90% of your risk capital. (investopedia.com)

External Links

How To

How to save money properly so you can retire early

Retirement planning is when you prepare your finances to live comfortably after you stop working. It's the process of planning how much money you want saved for retirement at age 65. It is also important to consider how much you will spend on retirement. This includes hobbies and travel.

You don't need to do everything. Many financial experts can help you figure out what kind of savings strategy works best for you. They will assess your goals and your current circumstances to help you determine the best savings strategy for you.

There are two main types, traditional and Roth, of retirement plans. Roth plans allow you put aside post-tax money while traditional retirement plans use pretax funds. It all depends on your preference for higher taxes now, or lower taxes in the future.

Traditional retirement plans

A traditional IRA allows pretax income to be contributed to the plan. If you're younger than 50, you can make contributions until 59 1/2 years old. If you wish to continue contributing, you will need to start withdrawing funds. The account can be closed once you turn 70 1/2.

If you already have started saving, you may be eligible to receive a pension. These pensions can vary depending on your location. Employers may offer matching programs which match employee contributions dollar-for-dollar. Some employers offer defined benefit plans, which guarantee a set amount of monthly payments.

Roth Retirement Plans

Roth IRAs have no taxes. This means that you must pay taxes first before you deposit money. When you reach retirement age, you are able to withdraw earnings tax-free. However, there are limitations. You cannot withdraw funds for medical expenses.

Another type of retirement plan is called a 401(k) plan. These benefits can often be offered by employers via payroll deductions. Extra benefits for employees include employer match programs and payroll deductions.

401(k), Plans

Employers offer 401(k) plans. These plans allow you to deposit money into an account controlled by your employer. Your employer will automatically contribute to a percentage of your paycheck.

You decide how the money is distributed after retirement. The money will grow over time. Many people choose to take their entire balance at one time. Others spread out distributions over their lifetime.

There are other types of savings accounts

Some companies offer other types of savings accounts. TD Ameritrade has a ShareBuilder Account. You can also invest in ETFs, mutual fund, stocks, and other assets with this account. You can also earn interest on all balances.

Ally Bank offers a MySavings Account. This account allows you to deposit cash, checks and debit cards as well as credit cards. You can also transfer money to other accounts or withdraw money from an outside source.

What next?

Once you are clear about which type of savings plan you prefer, it is time to start investing. Find a reliable investment firm first. Ask family and friends about their experiences with the firms they recommend. Online reviews can provide information about companies.

Next, you need to decide how much you should be saving. This is the step that determines your net worth. Net worth can include assets such as your home, investments, retirement accounts, and other assets. It also includes liabilities, such as debts owed lenders.

Divide your net worth by 25 once you have it. This number is the amount of money you will need to save each month in order to reach your goal.

For example, let's say your net worth totals $100,000. If you want to retire when age 65, you will need to save $4,000 every year.