One of most popular myths about credit is that it is determined according to your income. This myth is true to an extent, but it is not the most important. The next most important factor to consider is your credit utilization ratio. The best way to improve your credit score is by closing high interest accounts. This myth can jeopardize your credit score. In order to improve your score, you must use credit responsibly.

Your income is not a factor in determining your credit score

Many people don't know that your income isn't a factor in determining your credit score. While your income may be a factor when applying for credit, it doesn't reflect your ability to manage debt. When reviewing applications, lenders care more about your ability to manage debt than you income. You should still understand the reasons behind the decision, even if income is a factor.

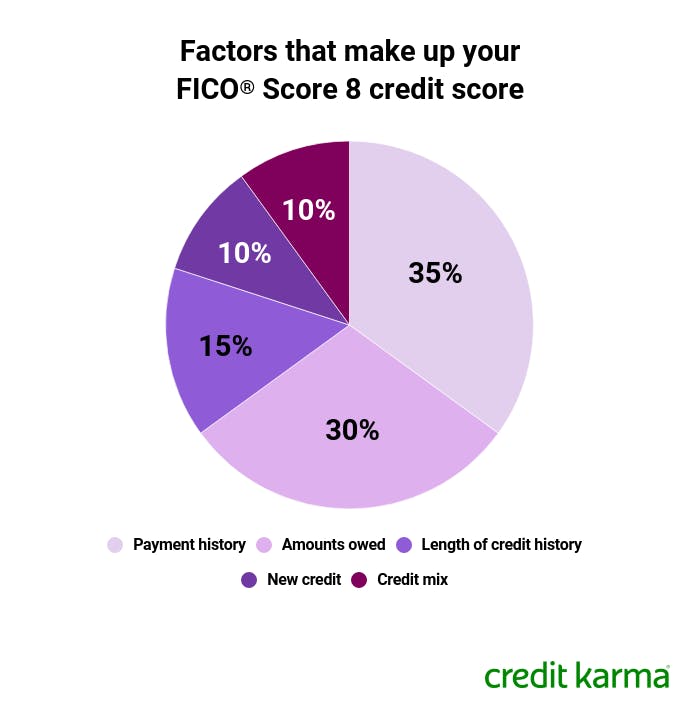

The next important factor that determines your credit score is your credit utilization ratio

Your credit utilization ratio is the next most important factor in determining credit score. This number is a measure of how much of your credit you use. Credit score can be improved by having less credit available, but it can also be affected if you have too much. There are some easy ways that you can increase your credit utilization ratio.

Closing old accounts with a high interest rate will increase your credit score

Credit accounts that are older than four years old can be a great way of improving your credit score. Keeping the average age of each account to around four years is beneficial to your FICO score. If you have many older credit cards, you should try to pay off the balance each month. This will increase your average age and FICO score. Do not open any new credit cards. Having too many accounts will negatively impact your FICO score.

Applying to for credit cards may affect your credit score

Applying for credit cards can temporarily lower your score but you can improve it quickly. The reason for this is that new application triggers a hard inquiry to your credit report. These information are used by credit scoring elves for calculating your credit score. This information pertains to how many applications you've made for credit cards in the last 12 months, but not the number.

Getting a credit score boost can cost you money

Even though it may seem expensive to get a credit rating boost, it could be well worth the investment if it means you will enjoy higher rates on everything from loans to credit cards. People with excellent credit receive better rates on all types credit cards and loans because they are seen as less risk. Poor credit is less attractive to lenders, and they are often subject to higher interest rates. Bad credit can make it difficult to rent housing, car rent, or get life insurance.

FAQ

Can I lose my investment?

Yes, you can lose all. There is no guarantee that you will succeed. There are however ways to minimize the chance of losing.

One way is to diversify your portfolio. Diversification helps spread out the risk among different assets.

You can also use stop losses. Stop Losses let you sell shares before they decline. This reduces your overall exposure to the market.

Finally, you can use margin trading. Margin Trading allows the borrower to buy more stock with borrowed funds. This can increase your chances of making profit.

How can I reduce my risk?

Risk management means being aware of the potential losses associated with investing.

One example is a company going bankrupt that could lead to a plunge in its stock price.

Or, a country's economy could collapse, causing the value of its currency to fall.

You could lose all your money if you invest in stocks

Therefore, it is important to remember that stocks carry greater risks than bonds.

One way to reduce your risk is by buying both stocks and bonds.

This increases the chance of making money from both assets.

Spreading your investments across multiple asset classes can help reduce risk.

Each class comes with its own set risks and rewards.

Stocks are risky while bonds are safe.

If you're interested in building wealth via stocks, then you might consider investing in growth companies.

Focusing on income-producing investments like bonds is a good idea if you're looking to save for retirement.

Do I really need an IRA

An Individual Retirement Account (IRA), is a retirement plan that allows you tax-free savings.

You can save money by contributing after-tax dollars to your IRA to help you grow wealth faster. You also get tax breaks for any money you withdraw after you have made it.

For those working for small businesses or self-employed, IRAs can be especially useful.

Many employers also offer matching contributions for their employees. So if your employer offers a match, you'll save twice as much money!

Statistics

- If your stock drops 10% below its purchase price, you have the opportunity to sell that stock to someone else and still retain 90% of your risk capital. (investopedia.com)

- 0.25% management fee $0 $500 Free career counseling plus loan discounts with a qualifying deposit Up to 1 year of free management with a qualifying deposit Get a $50 customer bonus when you fund your first taxable Investment Account (nerdwallet.com)

- An important note to remember is that a bond may only net you a 3% return on your money over multiple years. (ruleoneinvesting.com)

- Some traders typically risk 2-5% of their capital based on any particular trade. (investopedia.com)

External Links

How To

How to Invest In Bonds

Investing in bonds is one of the most popular ways to save money and build wealth. However, there are many factors that you should consider before buying bonds.

If you want to be financially secure in retirement, then you should consider investing in bonds. You may also choose to invest in bonds because they offer higher rates of return than stocks. Bonds could be a better investment than savings accounts and CDs if your goal is to earn interest at an annual rate.

You might consider purchasing bonds with longer maturities (the time between bond maturity) if you have enough cash. Investors can earn more interest over the life of the bond, as they will pay lower monthly payments.

There are three types to bond: corporate bonds, Treasury bills and municipal bonds. Treasuries bill are short-term instruments that the U.S. government has issued. They pay very low-interest rates and mature quickly, usually less than a year after the issue. Large companies, such as Exxon Mobil Corporation or General Motors, often issue corporate bonds. These securities usually yield higher yields then Treasury bills. Municipal bonds are issued by states, cities, counties, school districts, water authorities, etc., and they generally carry slightly higher yields than corporate bonds.

Consider looking for bonds with credit ratings. These ratings indicate the probability of a bond default. Higher-rated bonds are safer than low-rated ones. Diversifying your portfolio into different asset classes is the best way to prevent losing money in market fluctuations. This helps prevent any investment from falling into disfavour.